RUSH ENTERPRISES INC \TX\ (RUSHA)·Q4 2025 Earnings Summary

Rush Enterprises Q4 2025: EPS Beats Amid Truck Market Downturn, Declares $0.19 Dividend

February 17, 2026 · by Fintool AI Agent

Rush Enterprises (NASDAQ: RUSHA) delivered mixed Q4 2025 results, with EPS beating estimates by 1.8% while revenue slightly missed by 0.4% as the commercial vehicle industry continued its prolonged downcycle. The company declared a $0.19 per share quarterly dividend and reaffirmed its commitment to shareholder returns through its $150 million stock repurchase program. Shares fell 2.6% following the release, trading at $70.01, with aftermarket trades showing $69.00.

Did Rush Enterprises Beat Earnings?

Rush Enterprises delivered a narrow EPS beat despite challenging industry conditions:

For the full year 2025, revenues totaled $7.4 billion with net income of $263.8 million, or $3.27 per diluted share, compared to $7.8 billion in revenue and $304.2 million net income ($3.72 EPS) in 2024.

8-Quarter EPS Beat Streak: Rush has beaten EPS estimates for 8 consecutive quarters, demonstrating disciplined cost management through the industry downturn.

What Changed From Last Quarter?

Several notable shifts emerged in Q4 versus Q3 2025:

Key Developments:

- New stock repurchase program: $150 million authorized in December 2025, replacing exhausted prior program

- Network expansion: Added two IC Bus dealerships in Ontario, Canada and Rush Truck Centers – Nashville Central

- Improved Class 8 demand signals: Quoting activity and order intake increased late in Q4

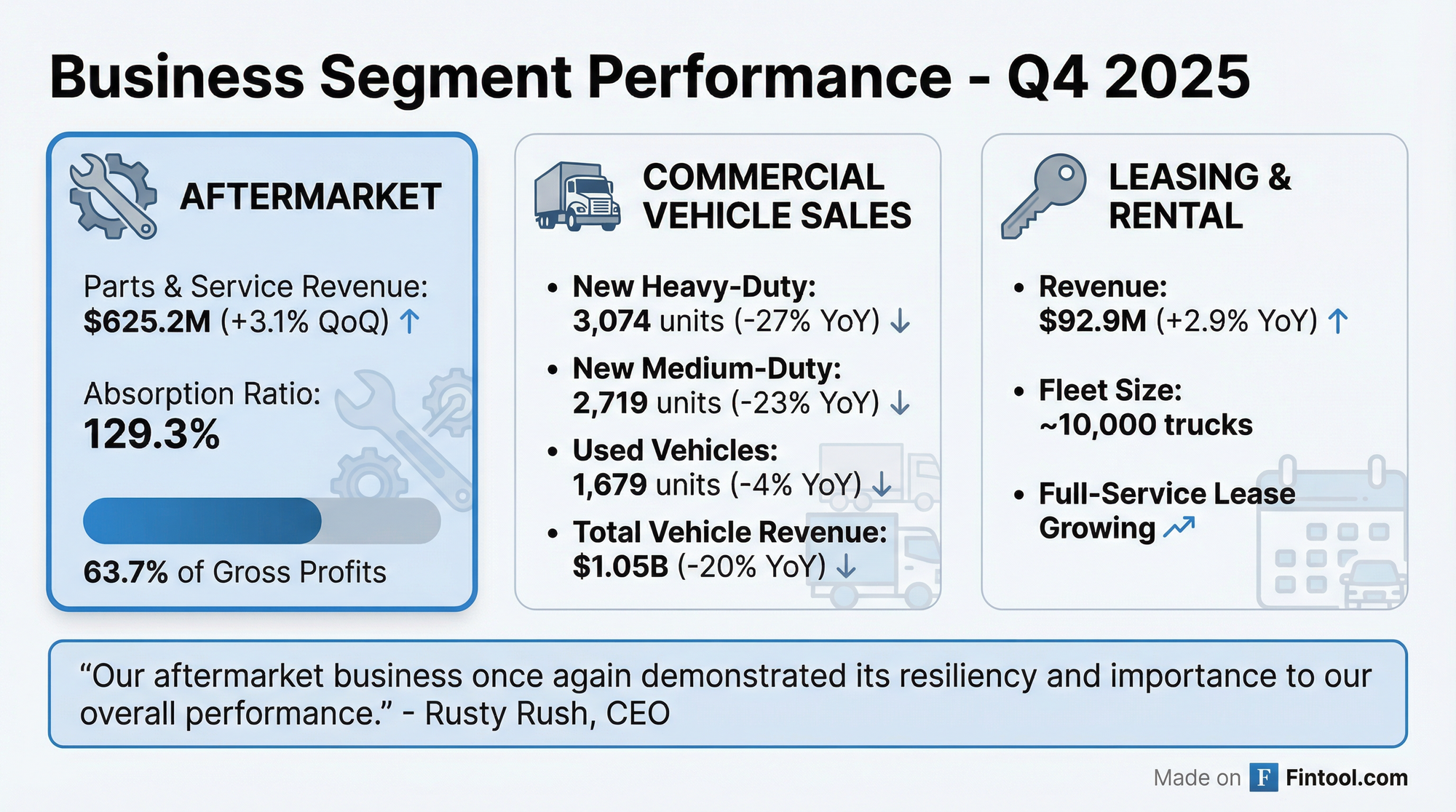

How Did Each Segment Perform?

Aftermarket Products & Services (The Resilience Story)

Aftermarket remained the profit engine, accounting for 63.7% of gross profits in 2025:

"Our aftermarket business once again demonstrated its resiliency and importance to our overall performance in 2025. Despite continued softness across the industry, we delivered stable aftermarket revenues and maintained a strong absorption ratio."

Commercial Vehicle Sales (Industry Headwinds)

New truck sales faced significant headwinds from depressed freight rates and fleet overcapacity:

For full-year 2025, Rush sold 12,432 new Class 8 trucks (down 17% YoY), capturing 5.8% U.S. market share.

Leasing & Rental (Steady Growth)

Rush Truck Leasing operates 55 franchises with approximately 10,000 trucks in its lease and rental fleet.

What Did Management Guide?

Rush does not provide specific numerical guidance, but management offered qualitative outlook:

Near-term (Q1 2026): "We expect industry conditions to remain challenging in the first quarter"

Full-Year 2026: Management is "cautiously optimistic about the remainder of the year" citing:

- Aging customer fleets beyond historical norms

- Increasing maintenance needs

- Signs of freight market improvement

- Increased clarity on tariffs and 2027 NOx emissions regulations

Industry Backdrop:

- ACT Research forecasts U.S. Class 8 retail sales of 211,300 units in 2026 (down slightly from 2025)

- Class 4-7 forecast of 218,225 units (up slightly)

Analyst Consensus for 2026:

Values retrieved from S&P Global

Capital Allocation & Shareholder Returns

Rush demonstrated commitment to returning capital despite the downcycle:

New Actions:

- $150M buyback program authorized December 2025 (through December 31, 2026)

- $0.19 quarterly dividend declared (up from $0.18) — payable March 18, 2026

"Our ability to return capital to shareholders through increased dividends and significant share repurchases, while maintaining a strong balance sheet and continuing to invest in the long-term growth of the business, reflects the resilience of our diversified operating model."

How Did the Stock React?

The stock had rallied significantly into earnings, up 53% from its 52-week low, potentially limiting upside even with the EPS beat.

Key Risks and Concerns

-

Prolonged freight recession: Over-the-road carriers continue facing depressed rates and excess capacity

-

Margin compression: Gross margin of 19.7% remains below the 20%+ levels seen in early 2024

-

Used truck pricing: "Market conditions were more difficult late in the year" though management believes pricing has stabilized

-

Regulatory uncertainty: 2027 NOx emissions standards pending EPA confirmation could drive pre-buy activity or further delays

Conference Call Details

Rush Enterprises will host its quarterly conference call on Wednesday, February 18, 2026, at 10:00 AM ET / 9:00 AM CT.

View earnings call transcript (available after call)

Data sourced from Rush Enterprises Q4 2025 8-K filing, S&P Capital IQ estimates. Stock data as of market close February 17, 2026.